- May 25, 2026

- 8 min read

- No Comments

Tax Planning Checklist for New Business Owners in California

Starting a business in California brings real excitement at first. Then tax notices appear, filing deadlines are imposed, and payroll rules and compliance requirements are thrust upon you. Many new owners pour their energy into sales, branding, hiring, and expansion while putting off tax planning at the outset. That choice usually leads to major money problems down the road.

California is one of the most complex states for business tax setups. And that is why skipping the filing of taxes, not maintaining the records, and payroll mistakes and forgotten deductions can really pile up in no time here. Then it results in fines, compliance issues, and extra taxes that could have been easily avoided.

Good tax planning goes beyond just getting returns in on schedule. It focuses more on consistent cash flow, compliance, organized finances, and tax savings.

A solid tax-planning checklist helps California companies stay ready, organized, and safe as they grow through every phase.

What is Tax Planning for Businesses?

Tax planning for businesses means arranging financial matters in a smart way to reduce additional tax costs while fully complying with all federal, California, and local tax rules.

Business tax planning includes:

- Entity structure planning

- Expense tracking

- Payroll tax management

- Quarterly tax preparation

- Deduction planning

- Financial recordkeeping

- Compliance management

- Year-end tax strategies

Importance of Tax Planning for New Business Owners in California

Helps Reduce Unnecessary Tax Liabilities

Smart tax planning allows businesses to identify potential tax deductions, properly organize business operations, and reduce unnecessary taxes before they accrue.

Improves Cash Flow Management

Businesses that do their tax planning properly prepare for quarterly taxes, payroll charges, and everyday expenses that can arise and thus won’t have any sudden cash crunches when the tax period rolls around.

Prevents Expensive Penalties and Compliance Issues

Penalties, interest, and official notices from tax offices can be issued quickly due to late filing, unpaid taxes, payroll errors, and poor record-keeping.

Supports Better Financial Organization

When California businesses are growing, they see the benefits of solid tax planning, as it helps hone their bookkeeping, financial reporting, and expense tracking, as well as their perspective on operations.

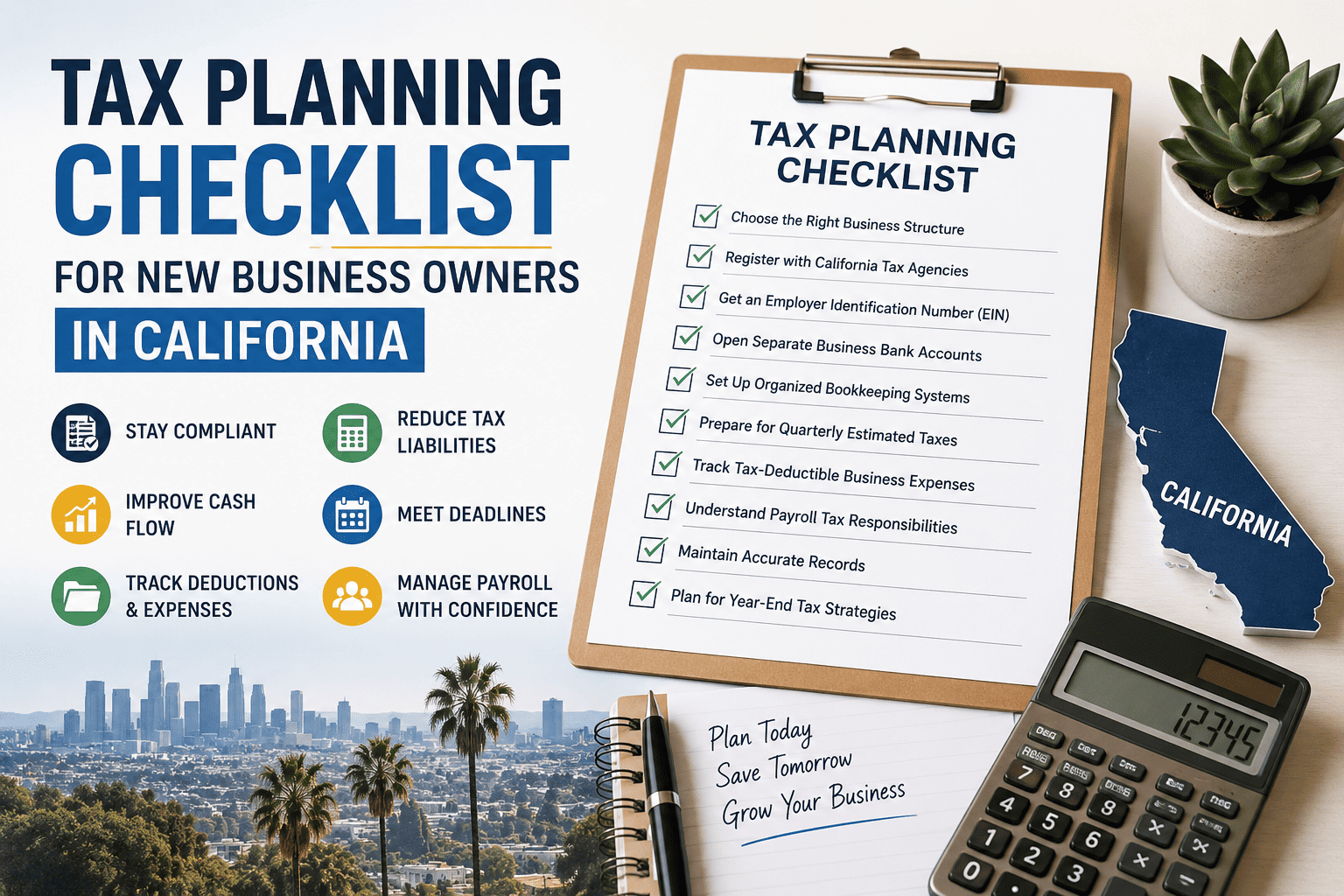

Tax Planning Checklist for New Business Owners in California

Throughout the year, new businesses in California handle numerous financial and compliance tasks. A clear checklist reduces tax risks, improves order, and maintains better financial control as the company scales.

Choose the Correct Business Structure

The selected entity affects taxes, liabilities, payroll obligations, and the future use of funds. Even in California’s challenging tax environment, owners should review LLCs, S corporations, sole proprietorships, partnerships, and C corporations before registering, as the wrong choice can be detrimental to their tax situation over time.

Register With California Tax Agencies Properly

Businesses may need to register with the California Department of Tax and Fee Administration, Employment Development Department, and Franchise Tax Board, depending on the type of business.

Failure to follow these steps may lead to compliance problems, late filings, payroll issues, sales tax problems, and a shock of penalties for a new business that may employ taxable workers or perform taxable work.

Apply for an Employer Identification Number (EIN)

An EIN will help ensure that personal and company funds remain distinct and make establishing and managing payroll, hiring employees, filing tax forms, banking, and reporting much simpler.

Having an EIN makes recordkeeping more accurate and tax handling simpler for companies that plan to grow, expand operations, or hire employees in California.

Open Separate Business Bank Accounts

Blending personal and business funds leads to messy accounting, missed deductions, compliance risks, and audit issues later on.

Companies should use separate checking and savings accounts, business credit cards, and accounting tools to improve money management, maintain accurate records, gain daily visibility, and make tax prep much easier.

Set Up Organized Bookkeeping Systems

Weak bookkeeping leads to some of the worst financial problems for small companies. Businesses should be careful when tracking revenues, payroll, operating expenses, vendor payments, receipts, invoices, and purchases.

Clear financial statements create more deduction opportunities, reduce filing errors, simplify reporting, and provide greater assurance in audits and reviews.

Prepare for Quarterly Estimated Tax Payments

In California, many businesses do not pay estimated taxes for the entire year but instead pay them in four installments.

These payments frequently result in interest, penalties, lack of cash and additional stress. Businesses will need to carefully work out their estimates to ensure that funds remain consistent throughout the year and do not come as a shock at tax time.

Track Every Tax-Deductible Business Expense

One of the issues that often arises is that companies pay more taxes than they should because they do not maintain accurate records of what they can deduct.

Common deductions include office expenses, marketing and advertising expenses, software expenses, insurance, professional assistance, equipment purchases, internet costs, travel expenses, and other business expenses. Clear records stay key for protecting deductions and handling audits.

Understand California Payroll Tax Responsibilities

When you hire employees, you have to deal with various payroll tax requirements, including federal withholding, California payroll taxes, unemployment taxes, employee reports, and compliance.

Payroll errors can lead to swift penalties and daily problems. Companies should establish reliable payroll systems early to remain compliant and maintain accurate employee reporting.

Register for Sales Tax if Required

Typically, locally required seller permits and sales tax returns are required if the company sells taxable goods or services. Failure to collect, report, and/or remit sales taxes can result in significant penalties and compliance issues.

There are fewer risks and fewer reporting problems for companies later on if they first understand the state’s sales tax regulations.

Maintain Compliance With California Franchise Tax Rules

Many LLCs and corporations in California pay annual franchise taxes even if they make no profit. Missing these payments can result in penalties, operational suspensions, and business restrictions. Companies should monitor franchise tax due dates closely and keep state filing rules in effect year-round.

Organize Financial Documents and Tax Records

Companies should keep clear copies of payroll reports, receipts, tax returns, bank statements, vendor invoices, contracts, and financial statements ready all year. Strong records protect the business in audits, improve report quality, ease tax prep, and support money orders as the company grows in California.

Plan Ahead for Year-End Tax Strategies

Leaving everything until tax season cuts down options to save money. Companies should review performance early to assess retirement contributions, equipment purchases, income timing, faster deductions, and tax credits before the year ends. Planning ahead lowers tax costs and gives owners more flexibility for future decisions.

Important Tax Deadlines California Businesses Should Track

California companies need to watch several filing dates throughout the year. Missing key dates often leads to penalties, interest, official notices, and business interruptions that hurt cash flow and future money orders for growing companies.

Quarterly Estimated Tax Deadlines

Businesses that must make estimated payments usually send them four times a year. Missing these dates often results in penalties, interest, and sudden financial pressure as the company grows.

California Franchise Tax Deadline

Many California LLCs and corporations pay annual franchise taxes no matter their profit level. Companies should monitor these dates to avoid penalties, suspensions, and issues with the California Franchise Tax Board.

Payroll Tax Filing Deadlines

Companies with staff file payroll taxes on set schedules based on their pay periods. Missing these dates can lead to big penalties, employee reporting problems, and quick compliance issues.

Sales Tax Filing Deadlines

Companies with sales tax registration file and pay collected taxes monthly, quarterly, or yearly, depending on their rules. Missing dates can create costly compliance issues and state penalties.

Federal and State Income Tax Return Deadlines

Companies prepare full federal and California tax returns each year on time and correctly. Late returns lead to penalties, delays, and extra financial pressure during key planning periods.

Common Tax Mistakes New California Business Owners Make

Mixing Personal and Business Finances

Combining personal and business transactions creates record confusion, deduction losses, incorrect reports, and higher audit risk when taxes are due.

Missing Quarterly Tax Payments

Many companies underestimate quarterly taxes early on, which leads to penalties, interest, and cash flow problems later.

Poor Expense Tracking

Lost receipts and incomplete records reduce the amount of valid deductions and lead to errors during tax filing.

Choosing the Wrong Business Structure

Choosing the wrong entity type can unnecessarily increase tax costs and create ongoing operational and financial drawbacks for future growth.

Ignoring California Compliance Requirements

One of the common and critical mistakes is failing to comply with California requirements, including overlooking payroll rules, franchise taxes, or sales tax duties. This often brings expensive compliance trouble fast.

Conclusion

Many California business owners do not realize how serious tax issues can become until penalties, official notices, payroll problems, or unexpected costs start to hurt daily operations. Weak records, missed dates, incorrect filings, and poor tax planning quietly undermine cash flow, profits, and future stability when the company needs them most. That is why solid tax planning should start right away.

Looking for a reliable tax consulting firm to help with tax planning? Kaya Tax & Bookkeeping Services, Inc. is among the leading tax and business consulting firms helping California business owners handle complex tax planning through expert tax planning, bookkeeping, payroll support, tax preparation, and compliance services designed for scalable companies.

Our team supports entrepreneurs in reducing unnecessary costs, avoiding costly mistakes, better organizing finances, and keeping operations steady year-round. Contact us today to stay compliant with the tax planning standard and focus on your business growth.